Market Commentary & Outlook First Quarter 2026

Q1

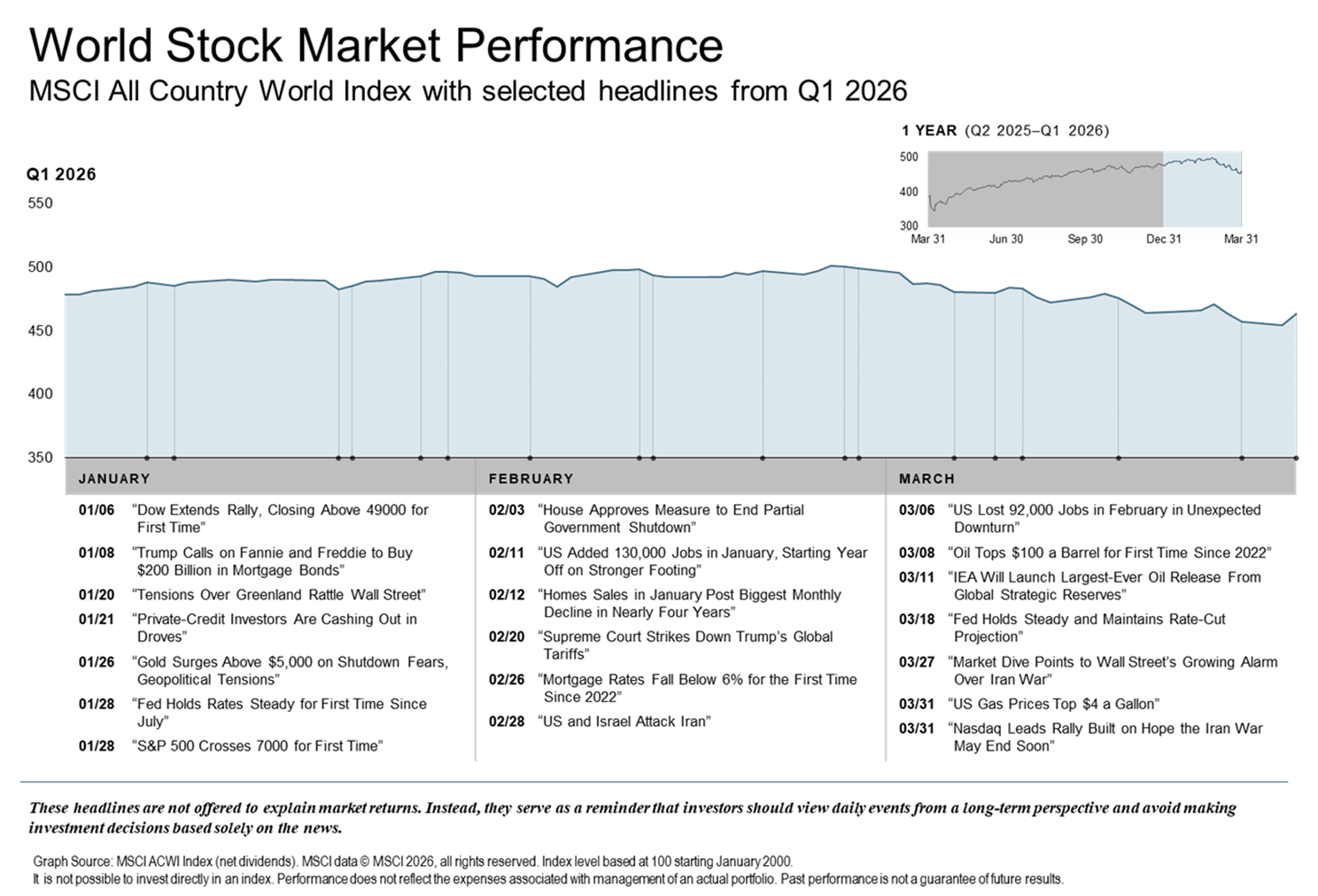

The Q1 economic climate can best be described as slowing but stable. As the year began, investors contemplated the implications of the AI boom. But, in contrast to the past couple of years, rather than AI driving a bull market, the focus shifted to the impact of AI on other businesses. The market started to price AI as a potential replacement of entire categories of professional services, not just a tool to make companies more efficient.

As the quarter progressed, the onset of the Iran war and the closure of the Strait of Hormuz led to surging oil prices and more uncertainty surrounding global financial markets. Higher oil prices contributed to a shift in rate cut expectations.

The mixed but ultimately resilient economic picture reflects an economy transitioning from above-trend growth to a more sustainable pace. Consumer spending remained the primary driver of growth despite confidence measures dipping early in the quarter in response to inflation concerns. Inflation continued to moderate with the Consumer Price Index falling to approximately 2.4% year-over-year in January while GDP estimates suggest growth in the 1.5% to 2% range. Technology and AI-related spending continued to be strong while certain cyclical industries, including the housing market, showed signs of softness.

Global Economy

Q1 showed a resilient yet fragile global economy with moderate growth that was uneven across regions. Despite inflation continuing to cool in many countries, central banks remained cautious with expected rate cuts delayed.

In Europe growth was weak to stagnant, especially in major economies such as Germany. As we head into Q2, the European Central Bank is staying cautious with expectations of eventual easing.

China experienced slower than expected growth despite government stimulus efforts. Weak consumer confidence is a major contributing factor as well as ongoing issues in the property sector.

Emerging markets performance was mixed with some countries benefiting from strong commodity exports.

Developed markets: -2.3%

Emerging markets nearly flat

U.S. Economy

The U.S. economy remains on solid footing, though growth is moderating. Although economic activity is slowing, it remains positive. The labor market has remained strong but hiring momentum is cooling slightly. Inflation is gradually declining while the Federal Reserve remains data-dependent.

U.S. Equity Markets

Markets have demonstrated resilience despite a complex backdrop that includes geopolitical tensions, evolving monetary policy expectations, and mixed economic data. After a period of volatility in March—driven in part by energy price shocks and geopolitical concerns—markets have rebounded as conditions stabilized.

At the end of Q1:

S&P 500: -4.3%

NASDAQ: -7%

Value Stocks outperformed growth stocks

Recent gains have been supported by:

Easing inflation data

Improved corporate earnings expectations (now projected near ~19% growth for 2026)

Renewed optimism surrounding geopolitical developments

Importantly, market leadership is beginning to broaden beyond a narrow group of mega-cap companies—an encouraging sign for overall market health.

Fixed Income

Fixed income markets were volatile but stable. Bond markets experienced volatility as yields rose across the curve. Short‑term yields moved higher in response to shifting Fed expectations, while longer‑term yields reflected both inflation uncertainty and a resilient economic backdrop. For investors, the fixed‑income landscape remains constructive: yields are at levels not seen in years, and high‑quality bonds continue to offer meaningful income and portfolio stability.

10-year U.S. Treasury closed near 4.43%

Commodities

Commodities were among the strongest‑performing asset classes this quarter, driven by geopolitical disruptions, supply constraints, and resilient global demand. Crude oil and natural gas prices surged as tensions in the Middle East disrupted shipping routes and raised concerns about supply reliability. Energy equities benefited significantly from this backdrop. Prices for copper and aluminum firmed as global manufacturing activity stabilized and infrastructure spending remained robust. Grain markets experienced volatility due to weather‑related supply concerns and shifting export patterns, though pricing remained generally elevated relative to historical averages.

Bloomberg Commodity Index (BCOM) rose 24.4%

Oil prices rose 73.5% year‑to‑date as of March 27

Looking Ahead

The outlook for 2026 has changed due to rising energy prices and the shift in investor expectations regarding Federal Reserve policy. Despite persistent inflation risks and the increase in geopolitical instability, many opportunities remain including: broadening market participation beyond mega-cap stocks, continued earnings growth supporting equities, and tactical opportunities in undervalued sectors. Historically, markets tend to look beyond military conflicts, and secular economic trends ultimately prevail.

Market Performance Snapshot (Through Mid-April 2026)

S&P 500: Recently trading near 6,950–6,970, just below all-time highs reached earlier this year

Year-to-Date Equity Trend: U.S. equities have recovered from a March pullback and are modestly positive for the year, supported by resilient earnings and improving sentiment

Nasdaq Composite: Strong momentum, including a recent 10-day winning streak, reflecting continued strength in growth and technology sectors

Dow Jones Industrial Average: Also trending higher, reflecting broader participation across sectors

Fixed Income:

10-Year U.S. Treasury Yield: Approximately 4.2%–4.3%, providing attractive income levels relative to recent years

2-Year Treasury Yield: ~3.7%–3.8%, reflecting expectations for a relatively stable policy rate environment

Our Perspective

We are aware that recent geopolitical tension has escalated investor apprehension. While uncertainty remains, moderating inflation, stable economic growth, and improved bond market dynamics create a more constructive backdrop for diversified portfolios.

We believe that maintaining a disciplined, long-term investment approach—focused on diversification, quality, and risk management—remains the most effective way to achieve your financial objectives.

As always, your portfolio is aligned with your individual goals and circumstances. If you would like to discuss your strategy in more detail, we welcome the opportunity to connect.